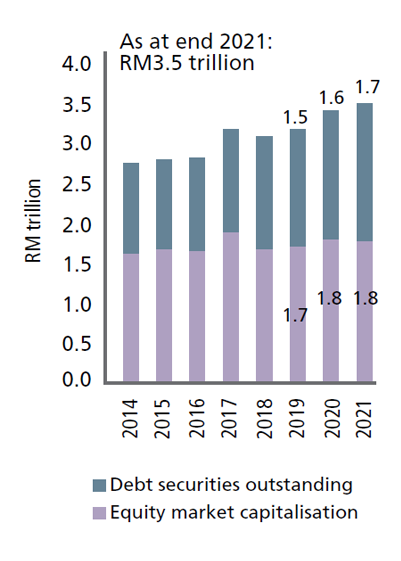

chart 3

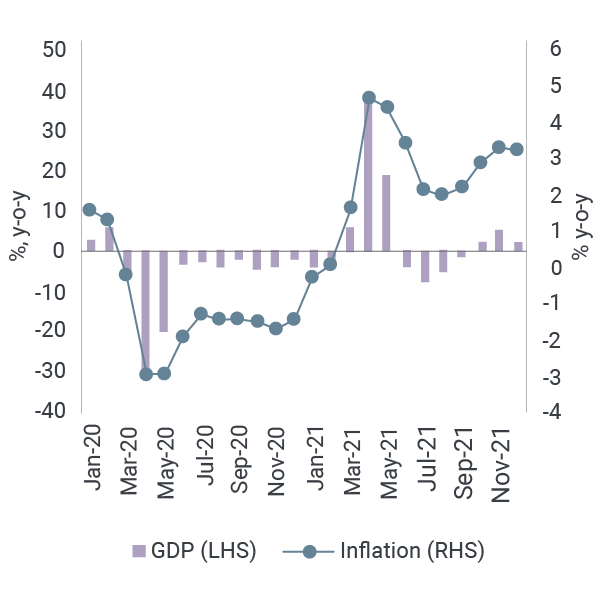

The Malaysian economy continued to recover in 2021, but a broad-based recovery was delayed by the worsening domestic COVID-19 situation mid-year

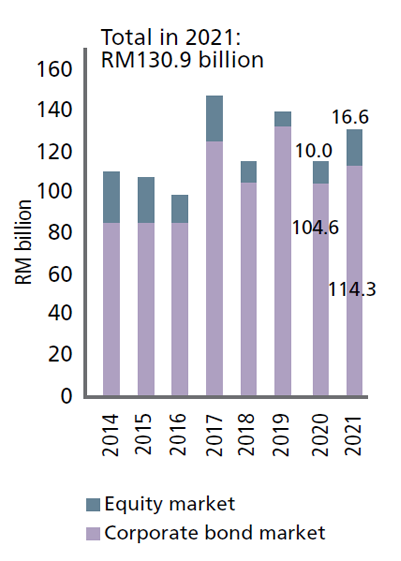

The Domestic Capital Market Continued To Support The Real Economy

The Malaysian capital market remained resilient and orderly throughout 2021 amid the relatively challenging global and domestic environment. Importantly, it continued to serve its fundamental roles in financing the domestic economy and intermediating savings. Total funds raised in the capital market remained robust, rising to RM130.9 billion in 2021 (2020: RM114.6 billion), above the five-year pre-pandemic average of RM121.4 billion, of which RM16.6 billion was raised via the equity market1, while RM114.3 billion was raised through the corporate bond market.

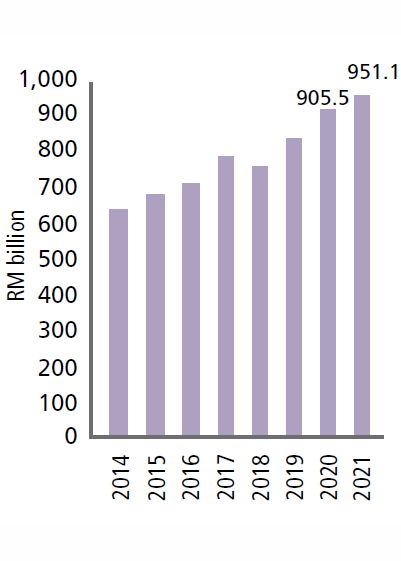

Meanwhile, alternative financing avenues2 via equity crowdfunding (ECF) and peer-to-peer financing (P2P financing) continued to gain traction, especially in supporting the funding needs of MSMEs. Likewise, the fund management industry grew further during the year, with AUM totalling RM951.1 billion (2020: RM905.5 billion). This mainly reflects increased diversification of financial assets in domestic and foreign markets, with the unit trust segment3 remaining the largest source of funds for AUM. Overall, the size of the capital market rose to RM3.5 trillion in 2021 (2020: RM3.4 trillion).

chart 4

Despite a challenging environment, the capital market continued to support the economy, with steady growth in funds raised and AUM in the fund management industry

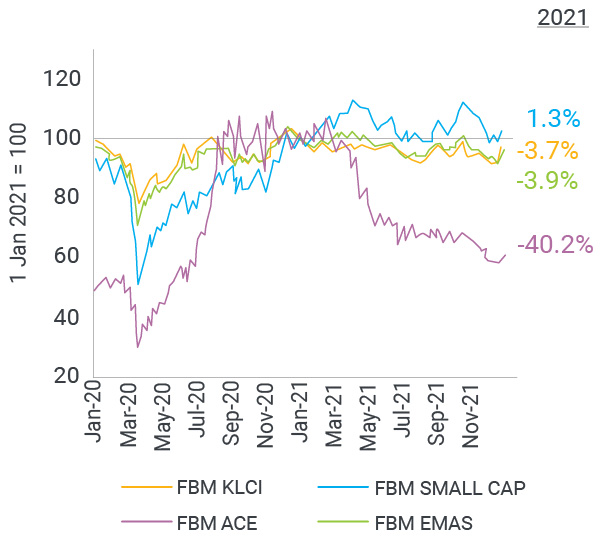

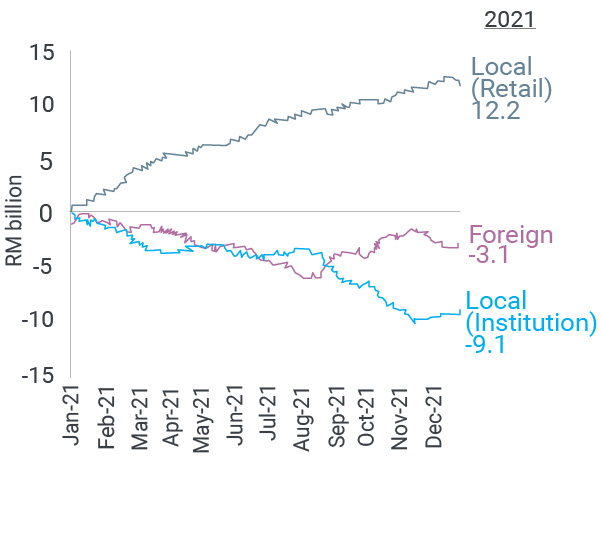

The domestic equity market was affected by continued headwinds both globally and domestically. The overall market capitalisation of Bursa Malaysia and the FBMKLCI moderated to RM1.79 trillion and RM1.04 trillion respectively in 2021 (2020: RM1.82 trillion and RM1.06 trillion respectively). Likewise, the FBMKLCI index declined by -3.7% to end the year at 1,567.5 points. Nevertheless, sentiments in the domestic equity market remained in favour of FBM Small Cap companies, given their continued outperformance during the year. In terms of trade participation, local institutions turned net sellers to a total of -RM9.1 billion in 2021, while net selling by non-residents eased to -RM3.1 billion (2020: -RM24.6 billion). Correspondingly, net buying by local retail investors rose to RM12.2 billion. The participation rate for retail investors thus was higher in 2021, rising to an average of 34.6% in terms of value traded.

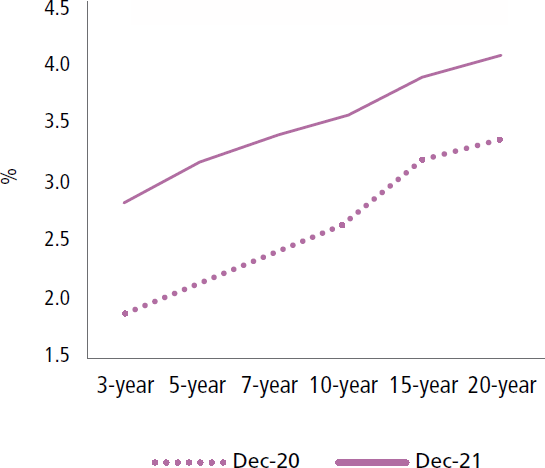

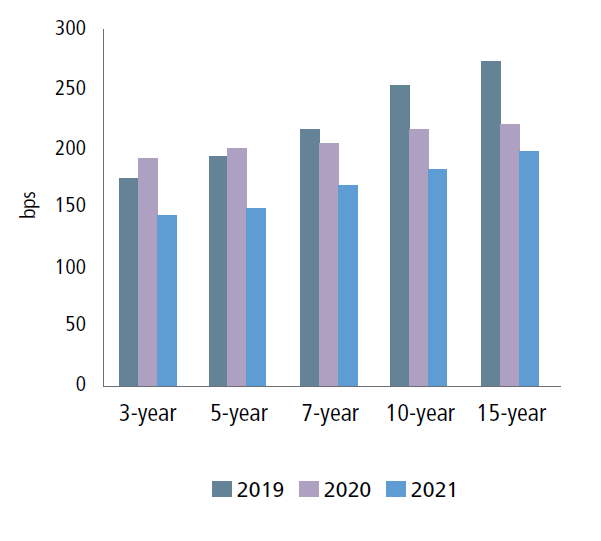

In the Malaysian bond market, total bonds outstanding grew to RM1.7 trillion in 2021 from RM1.6 trillion in 2020, reflecting higher levels of debt fundraising. The overall Malaysian Government Securities (MGS) yield curve broadly shifted upwards, led by mid-to long-term tenures, in tandem with the general increase in global bond yields amid higher global inflation expectations and the prospect of faster global monetary policy normalisation. Meanwhile, the spread between corporate bonds and MGS broadly narrowed across tenures, suggesting improved optimism on the domestic growth outlook especially towards the end of 2021. The domestic bond market also witnessed increased foreign interest, with net inflows amounting to RM33.6 billion in 2021 (2020: RM18.3 billion), the highest since 2012.

For further information on quarterly performance, please refer to SC Quarterly Report: Market Overview.

chart 5

The domestic equity market was affected by continued headwinds both globally and domestically in 2021

Note: * FBMKLCI consists of the largest 30 companies ranked by full market capitalisation in the FTSE Bursa Malaysia EMAS Index; FBM Small Cap consists of all constituents of the FTSE Bursa Malaysia EMAS Index that are not constituents of the FTSE Bursa Malaysia Top 100 Index; and FBM ACE comprises all companies listed on the ACE Market.

chart 6

MGS bond yields experienced upward pressure across tenures, tracking global bond markets