The AOB’s key oversight activities such as registration, inspection and enforcement are aimed at promoting high

quality audit practices. The AOB encourages that audit firms build capacity and have in place quality framework which

enables quality audits to be performed consistently.

The AOB’s oversight activities are targeted to:

table 1 - Registered and recognised auditors as at 31 December 2022

Profile of audit firms | No. of audit firms | No. of individual auditors | No. of PIE audit client | % of total market capitalisation | No. of schedule fund audit clients | % of total net asset value |

|---|---|---|---|---|---|---|

| Registered audit firms | ||||||

| Partnerships with 10 and more audit partners | 10 | 249 | 995 | 96.44 | 1,272 | 98.56 |

| Partnerships with 5 – 9 audit partners | 14 | 71 | 153 | 2.60 | 21 | 1.31 |

| Partnerships with fewer than 5 audit partners | 12 | 37 | 75 | 0.83 | 20 | 0.13 |

| Sub Total | 36 | 357 | 1,223 | 99.87 | 1,313 | 100 |

| Recognised foreign audit firms | 4 | 12 | 5 | 0.13 | - | - |

| TOTAL | 40 | 369 | 1,228 | 100% | 1,313 | 100 |

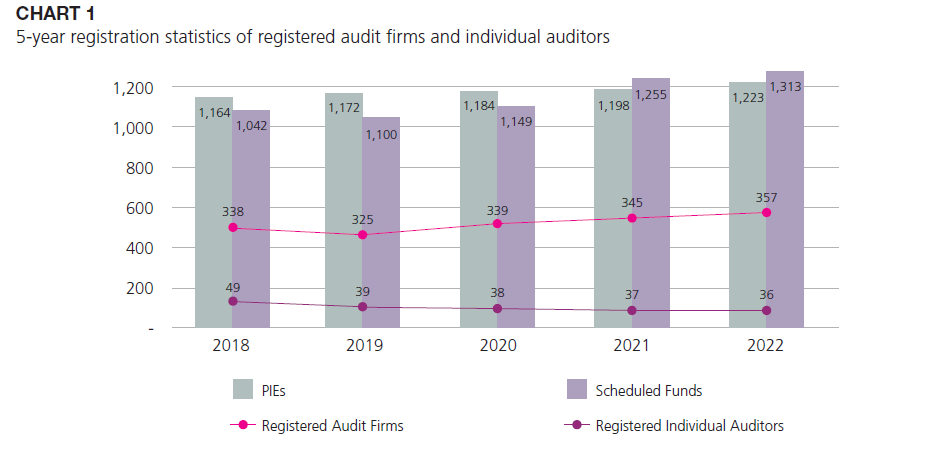

Chart 1 tabulates the number of registered audit firms and individual auditors for the past five years. The number of registered audit firms has decreased from 49 in 2018 to 36 in 2022. The sharp decrease in the number of audit firms was due to the AOB’s condition of registrations introduced in August 2018. The AOB tightened the conditions of registration in 2019 to improve and strengthen the audit firm’s internal capacity and governance. The registration conditions provided an avenue for the audit firms to restructure their practices to be better equipped to audit PIEs and schedule funds.

The number of registered individual auditors has steadily been increasing since 2019 as audit firms have been building capacity.

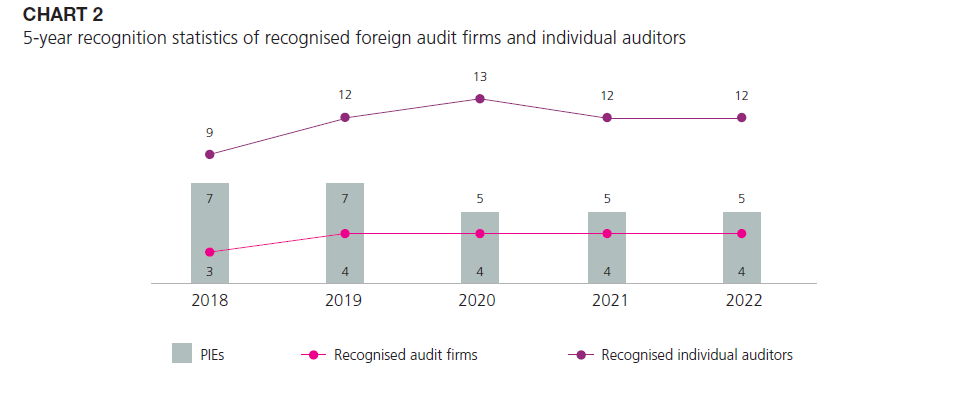

Chart 2 tabulates the number of recognised audit firms and individual auditors for the past five years. Over the years, the number of recognised audit firms and individual auditors have remained steady at four recognised firms and 12 individual auditors.

The recognised audit firms are from Singapore, Hong Kong and the UK. Recognised audit firms must be an internationally affiliated network firm, with effective technical support and robust quality control from its network firm.

The AOB relies on the oversight frameworks of the recognised auditors’ home jurisdictions to determine whether they are fit and proper to audit PIEs. Part of this is ensuring that the audit firms comply with international quality control, auditing, ethical and other assurance standards, and that they are subjected to regular inspection by their home audit regulators.

PIE CLIENTS’ MOVEMENTS

Throughout 2022, an additional of two AOB registered audit firms with a total of 162 PIE clients met the criteria of Major Audit Firms. At present, Major Audit Firms in Malaysia consist of eight AOB registered audit firms which collectively audit 95.3% of the total market capitalisation of PLCs in Malaysia. Throughout 2022, there were new additions to the PIE client lists of the registered audit firms. Also, there were PLCs that were delisted and PIEs that were no longer considered PIEs.

As shown in Table 2 below, PIE audit clients continued to move from Major Audit Firms to Other Audit Firms in 2022. The AOB viewed the trends positively as the movement would dilute the market concentration in the audit industry.

While the AOB views this trend positively, Other Audit Firms are reminded to build up their respective firms’ human resources capacity from time to time to so as to uphold their audit quality. Other Audit Firms should keep abreast with the developments in the capital market. This is to ensure that the audit firms have the capable and competent resources to perform quality audits.

TABLE 2 - Clients’ movement among registered and recognised audit firms during year 2022

AGE PROFILE OF AOB REGISTERED AND RECOGNISED INDIVIDUAL AUDITORS

In 2017, the AOB highlighted the need for audit firms to consider the continuity and sustainability of its audit practice. Succession planning is important to minimise disruption to the practice and allow for a smooth exit and transition of the retiring partners. Audit firms must continuously recruit new talent, develop, mentor and groom their team members for management and leadership roles.

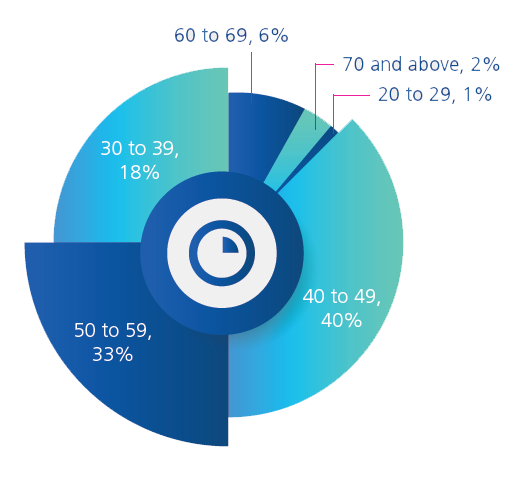

CHART 3 - Age profile of registered individual auditors as at 31 December 2022

Based on data in 2022, 41% (2017: 42%) of registered individual auditors are of the age of 50 years and above. Within this group,

20% (2017: 36%) are of the age of 60 years and above.

The oldest registered individual auditor is 79 years old. It is encouraging to note that the group with the age of 40 years and below has increased to 19% (2017:11%), indicating an increase in the number of younger talent in the profession.