DEVELOPMENT AND IMPLEMENTATION OF STANDARDS AND REGULATIONS

Development of accounting and auditing standards and their ensuing implementation are critical to raise the bar on audit quality.

In line with its efforts to influence audit quality by strengthening the accounting profession, the AOB participates as an observer in meetings held by the Auditing and Assurance Standards Board (AASB) and the Ethics Standards Board (ESB) of the Malaysian Institute of Accountants (MIA).

The AOB helps to bridge the gap between the industry and profession in understanding different challenges arising from current accounting and auditing issues, and also contribute its views on areas of concern.

To support the implementation of the IFRS Sustainability Disclosure Standards (ISSB Standards) and sustainability assurance standards in Malaysia, the Advisory Committee on Sustainability Reporting (ACSR) was established. The ACSR is chaired by the SC, and comprises representatives from BNM, Bursa Malaysia, the Companies Commission of Malaysia (SSM), the Financial Reporting Foundation and the AOB.

In October 2023, the SC hosted a global roundtable on the IAASB exposure draft, Proposed International Standard on

Sustainability Assurance (ISSA) 5000 General Requirements for Sustainability Assurance Engagements. The ISSA 5000

global roundtable was participated by preparers of sustainability information, sustainability reporting standard-setters,

assurance practitioners, professional bodies and regulators from the Asia-Pacific region. During the event, the AOB has shared perspectives on the adoption of sustainability assurance standards.

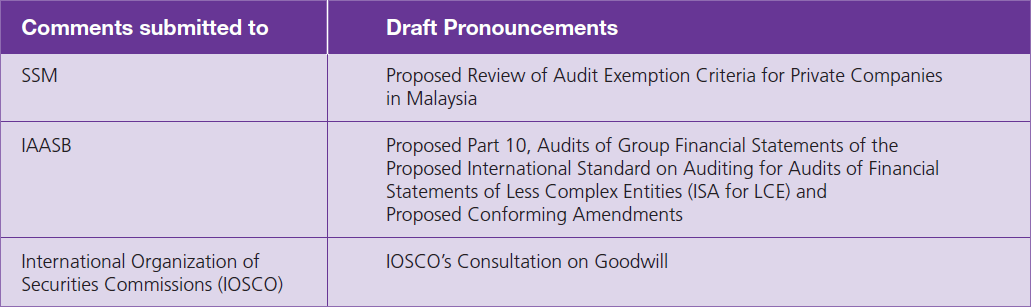

During the year, the AOB has also shared comments on various draft pronouncements as shown in Table 1.

IOSCO Consultation on Goodwill

In June 2023, IOSCO issued a consultation paper on goodwill to collect views from issuers, audit committees, investors and auditors.

It was observed that since the financial crisis, the total balance of accumulated goodwill of the S&P 500 has more than doubled from US$1.6 trillion in 2008 to US$3.7 trillion in 2021, and the accumulated goodwill of listed companies in the European Union is also having the same increasing trend. The rise was because of active merger and acquisition activities with high acquisition prices.

Goodwill is subject to an impairment test annually and no amortisation under the current global accounting standard. Goodwill is impaired when its recoverable amount is lower than its carrying amount. Some stakeholders were concerned that optimistic assumptions were used in estimating the recoverable amount and resulted in impairment loss not being recognised adequately and timely.

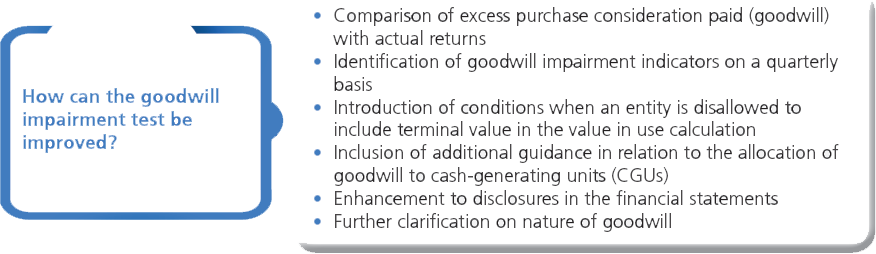

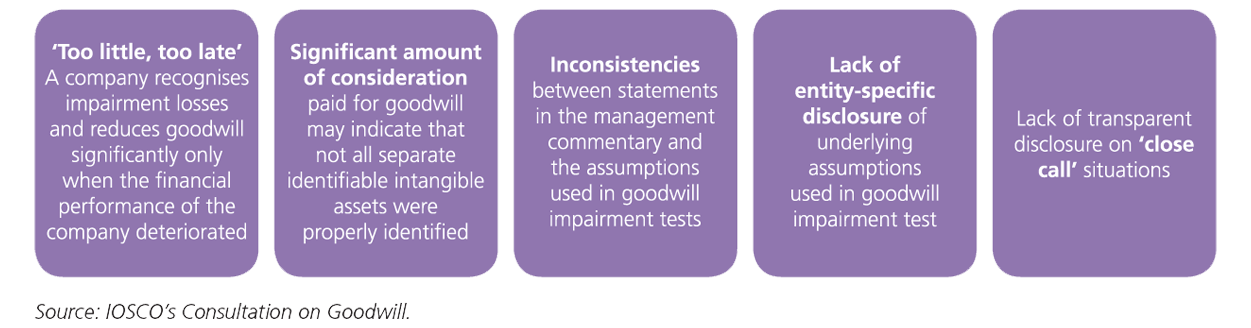

While supporting the IASB’s plan to enhance disclosure requirements on acquisition and its subsequent performance, IOSCO is of the view that goodwill impairment could be further improved. IOSCO’s observations on issues surrounding goodwill are depicted in Figure 1.

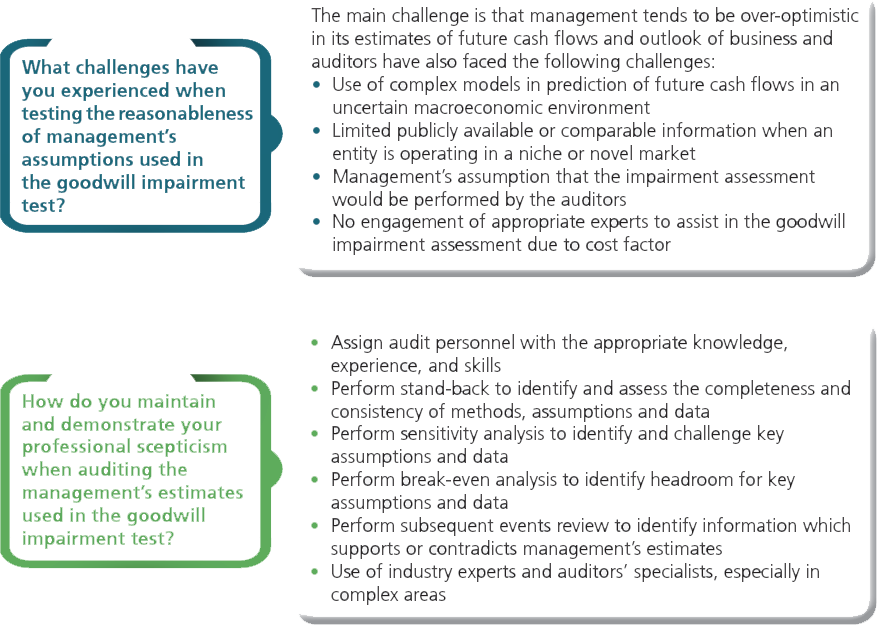

During the AOB’s Annual Conversation with Major Audit Firms, the AOB provided brief backgrounds on IOSCO’s Consultation on Goodwill and sought views on questions related to auditors. The consolidated auditors’ responses to IOSCO’s Consultation on Goodwill – Questions for Independent Auditors are summarised in Figure 2.

FIGURE 1

IOSCO’s observations on issues surrounding goodwill

FIGURE 2

Compiled auditors’ responses to IOSCO’s Consultation on Goodwill – Questions for independent auditors