Page 236 - SC SCAR 2023 ENGLISH Flipbook

P. 236

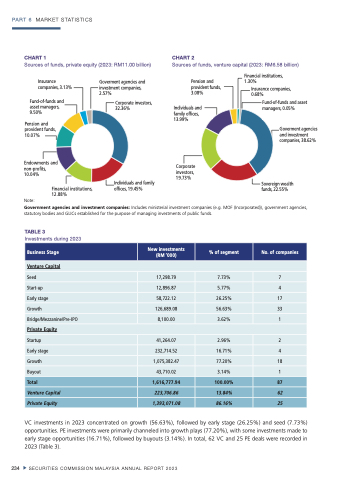

PART 6 MARKET STATISTICS

CHART 1

Sources of funds, private equity (2023: RM11.00 billion)

CHART 2

Sources of funds, venture capital (2023: RM6.58 billion)

Insurance companies, 3.13%

Fund-of-funds and asset managers, 9.50%

Pension and provident funds, 10.07%

Endowments and non-profits, 10.04%

Financial institutions,

12.88%

Goverment agencies and investment companies, 2.57%

Corporate investors, 32.36%

Individuals and family offices, 19.45%

Pension and provident funds, 3.08%

Individuals and family offices, 13.99%

Corporate investors, 19.73%

Financial institutions, 1.30%

Insurance companies, 0.68%

Fund-of-funds and asset managers, 0.05%

Goverment agencies and investment companies, 38.62%

Sovereign wealth funds, 22.55%

Note:

Government agencies and investment companies: Includes ministerial investment companies (e.g. MOF (Incorporated)), government agencies, statutory bodies and GLICs established for the purpose of managing investments of public funds.

TABLE 3

Investments during 2023

Business Stage

New investments (RM ‘000)

% of segment

No. of companies

Venture Capital

Seed

17,298.79

7.73%

7

Start-up

12,896.87

5.77%

4

Early stage

58,722.12

26.25%

17

Growth

126,689.08

56.63%

33

Bridge/Mezzanine/Pre-IPO

8,100.00

3.62%

1

Private Equity

Startup

41,264.07

2.96%

2

Early stage

232,714.52

16.71%

4

Growth

1,075,382.47

77.20%

18

Buyout

43,710.02

3.14%

1

Total

1,616,777.94

100.00%

87

Venture Capital

223,706.86

13.84%

62

Private Equity

1,393,071.08

86.16%

25

234

SECURITIES COMMISSION MALAYSIA ANNUAL REPORT 2023

VC investments in 2023 concentrated on growth (56.63%), followed by early stage (26.25%) and seed (7.73%) opportunities. PE investments were primarily channeled into growth plays (77.20%), with some investments made to early stage opportunities (16.71%), followed by buyouts (3.14%). In total, 62 VC and 25 PE deals were recorded in 2023 (Table 3).