INTRODUCTION

The Securities Commission Malaysia (SC) leverages behavioral insights to improve its regulatory outcomes, policy adjustments, and investor empowerment initiatives. Currently, there is a perceived lack of participation by Malaysian youth in the capital market. Thus, this research was conducted to provide insight into youths’ participation in the capital market. The findings will be used to guide the SC’s direction moving forward.

RESEARCH OBJECTIVES

KEY OBSERVATIONS AND FINDINGS

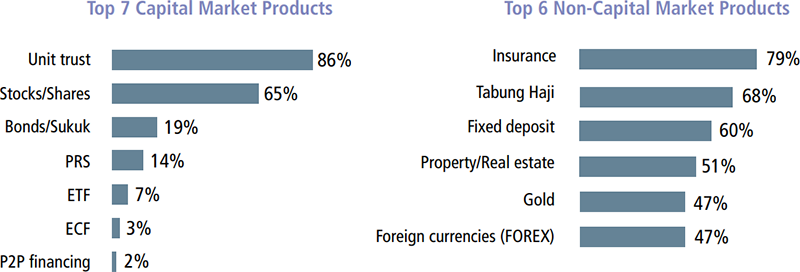

Youth awareness of capital market products

Overall the respondents were more aware of non-capital market product such as insurance, Tabung Haji, and fixed deposits, compared to capital market products. On respondents’ awareness of capital market products, unit trust and stock/shares were the highest at 86% and 65% respectively.

FACTORS CONSIDERED BEFORE INVESTING

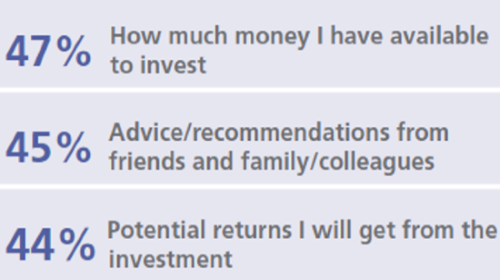

Respondents considered several factors prior to investing, such as being aware of how much money was available for them to invest, advice/recommendations from friends and family, including the potential returns of the investment. This shows that those with low disposable income would find it more difficult to set aside money for investment, especially when paired with risk concerns.

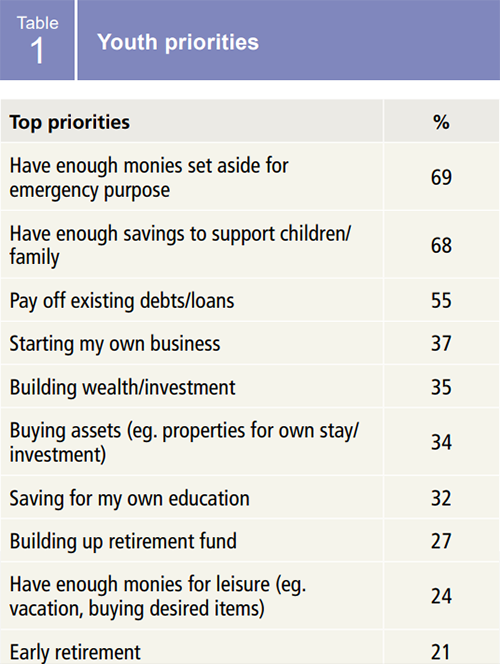

YOUTH'S PRIORITIES

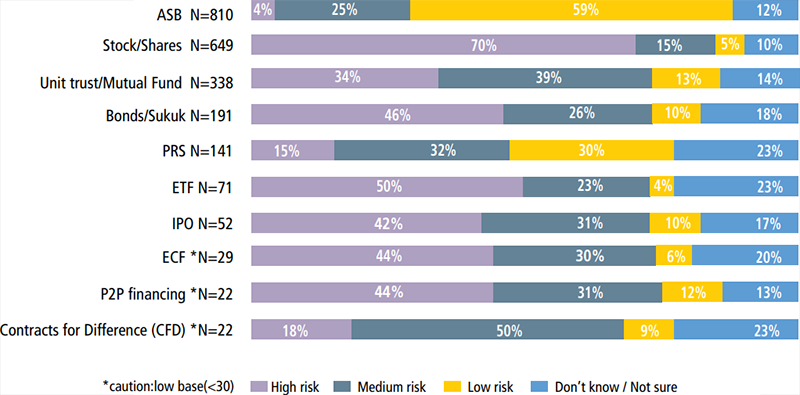

YOUTH’S PERCEPTION TOWARDS RISK

When respondents were asked on the level of risk that they were willing to take for their ideal investment, only 3% considered themselves to have a high-risk appetite.

Have a High risk appetite

Have a Medium to Low risk appetite

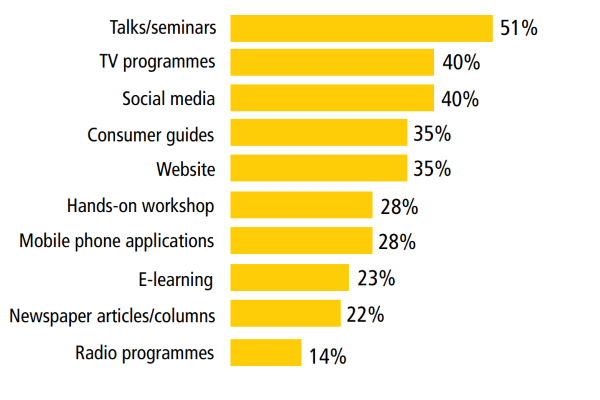

PREFERRED LEARNING METHOD