Proactive and robust surveillance and supervisory function and capabilities are important to ensure proper conduct and practices by market participants while maintaining trust in the capital market. Following the identified emerging risks and concerns in 2021, the SC carried out regulatory activities and initiatives aimed towards strengthening and broadening its supervisory and surveillance capabilities.

Fostering Resilience of Markets, Infrastructures and Institutions through Ongoing Monitoring and Supervision

Technology is central to efforts in promoting a fair, orderly, and transparent operation of market infrastructure. As IT infrastructure and systems become increasingly automated, interconnected and complex over time, the robustness and resilience of market technology, associated systems and processes are critical. As the only authorised integrated exchange in Malaysia, Bursa Malaysia is expected to offer the public a trading platform that is reliable, efficient, and transparent.

For information on the Regulatory Assessment on Bursa Malaysia, please refer to Figure 3.

Following the announcement in 2020 on the migration of the entire ACE market framework, including registration of prospectuses to Bursa Malaysia, the relevant rules and operational framework were put in place.

Bursa Malaysia will assume the role as a one-stop centre for the ACE market, effective 1 January 2022.

Monitoring of regulated short selling activities

On 4 January 2021, regulated short selling (RSS) activities resumed after being temporarily suspended for nine months since March 2020. Upon resumption of trading, renewed risk management activities resulted in fairly active RSS trades before moderating to an average of about 1% of the total market value traded throughout 2021. In addition, developments surrounding the GameStop short squeeze incident by retailers in the US gave rise to concerns over similar risks associated with domestic short-selling activities. However, such risks did not materialise in the domestic market given its different environment and regulatory framework including prescribed limits on short selling positions, among others.

Notwithstanding, the SC closely monitored RSS activities to ensure that transactions were carried out in a fair and orderly manner, and that emerging risks were effectively managed. Overall, RSS activities were well governed with enhanced and existing control measures in place to ensure market stability and mitigate against risks of excessive net-short positions. Such controls include tighter aggregate net-short position limits, trading tick rules, and daily short selling volume limits.

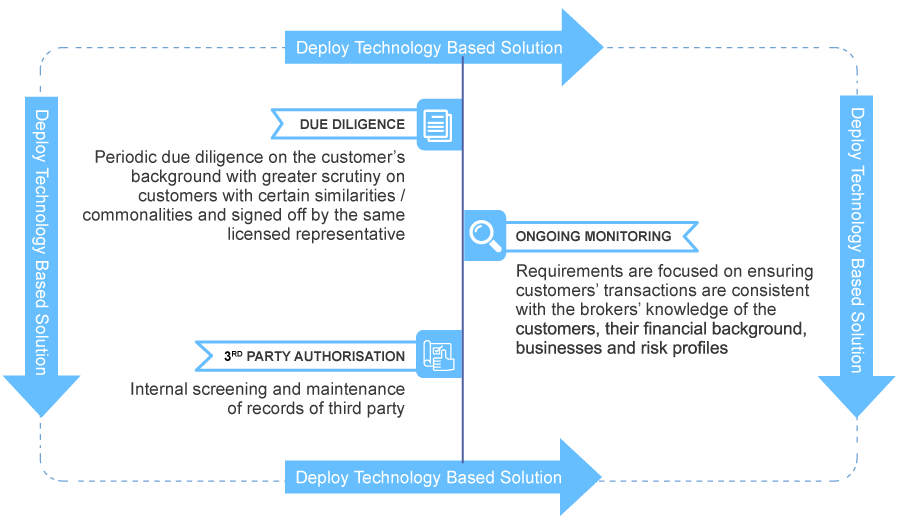

Enhancing off-site monitoring of market intermediaries

These Guidance Notes and communications outline best practices, clarifications, and areas where intermediaries should pay special attention or heighten their monitoring.