In accordance with Section 31V(1) of Part IIIA of the SCMA, the AOB conducts inspections on auditors of PIEs and schedule funds with the objective to promote high quality audits and reliable audited financial statements.

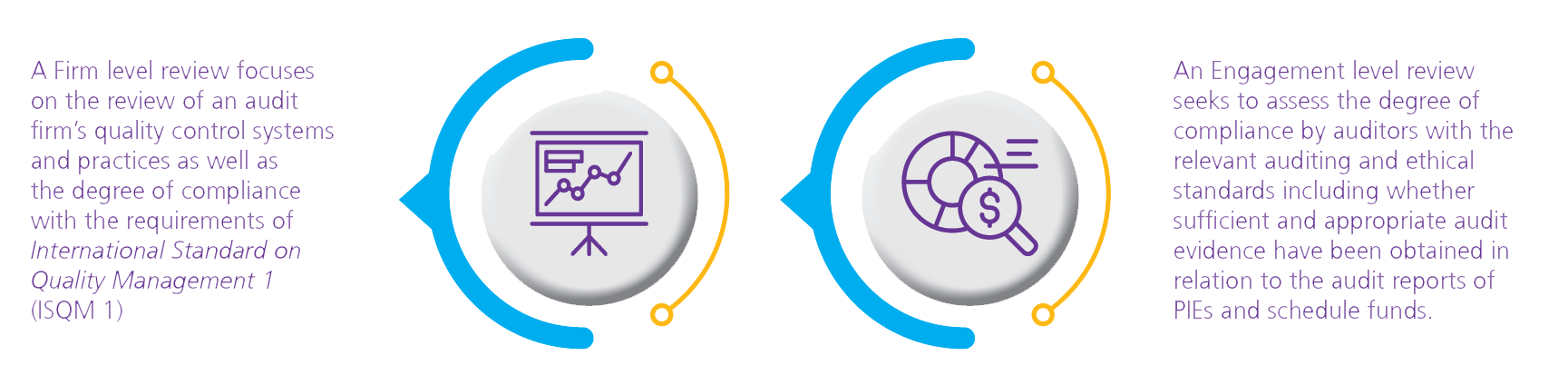

Inspections conducted by the AOB comprise Firm and Engagement level reviews.

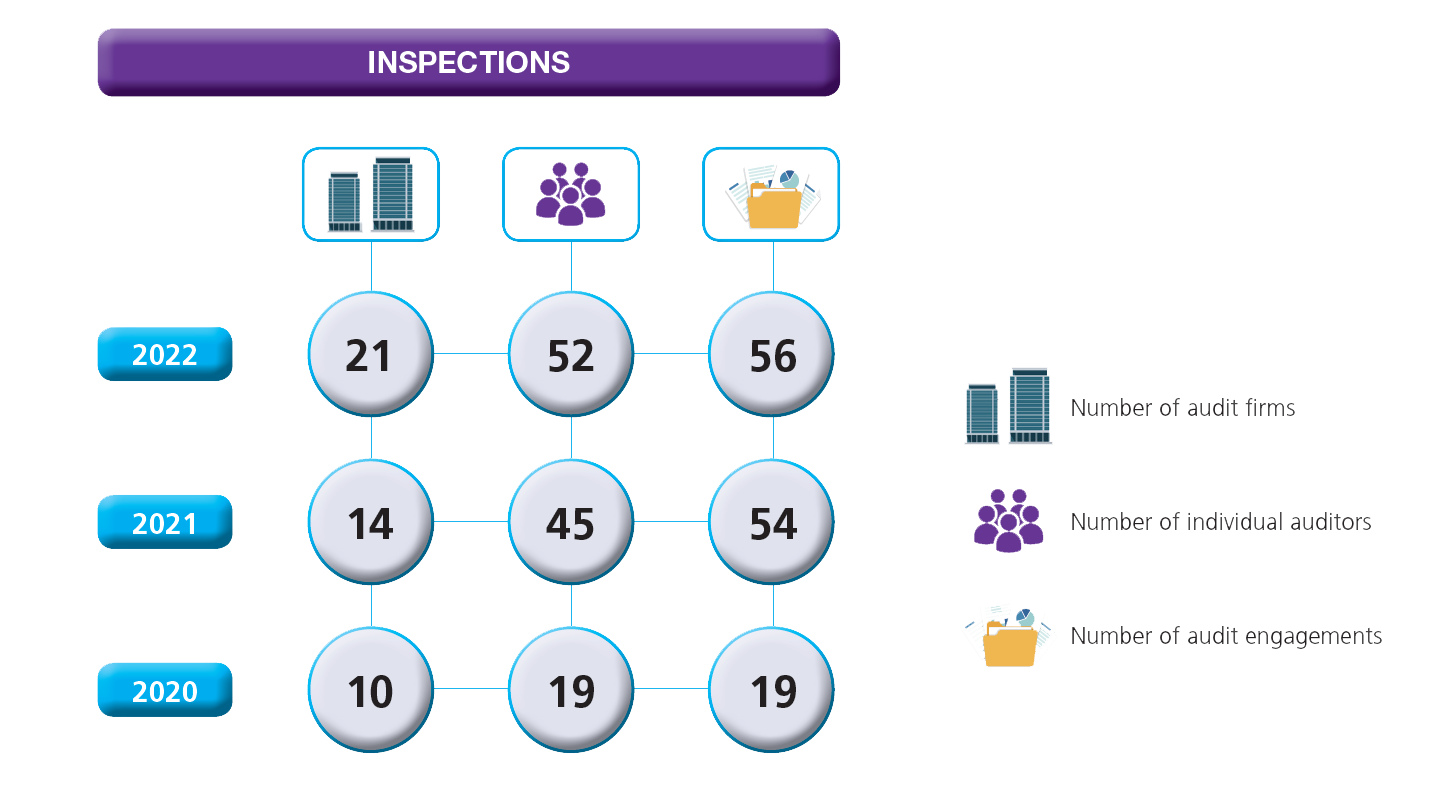

In 2022, the AOB inspected 21 Audit Firms covering 52 individual auditors for 56 audit engagements.

Each year, the AOB conducts inspections on all firms that have more than 50 PIE audit clients with a total market capitalisation of the PIE audit clients of above RM15.0 billion. These eight Major Audit Firms (2021: six Major Audit Firms) collectively audited PLCs that represented 73.5% of the total number of PLCs and 95.3% of the total market capitalisation of PLCs in Malaysia.

The AOB adopts a risk-based approach in selecting other audit firms for inspection under its monitoring programme.

The AOB takes into consideration various factors such as:

The AOB also conducted a number of targeted inspections to respond to emerging risks in a timely manner.

At the conclusion of every inspection, the AOB assesses the severity of findings arising from each engagement review. All findings are expected to be remediated by the audit firms within a timeline agreed with the AOB regardless of whether subsequent enforcement action is taken on the individual auditor or his/her firm.

The AOB emphasises the importance of identifying the actual root causes when putting in place a remedial action plan. It is essential that the remediation plan is holistic, relevant, and viable to ensure that any shortfall or weaknesses in audit quality are appropriately and promptly rectified to ensure high quality and reliable audited financial statements of PIEs and schedule funds.

More in-depth information on the inspection programme, including common inspection findings, results of thematic reviews, trends analysis and remediation efforts taken by inspected audit firms will be made available separately in the 2022 AOB AIR.

2022 INSPECTION HIGHLIGHTS

Risk-based approach taken by the AOB in the planning and engagement selection for its inspections and monitoring programmes

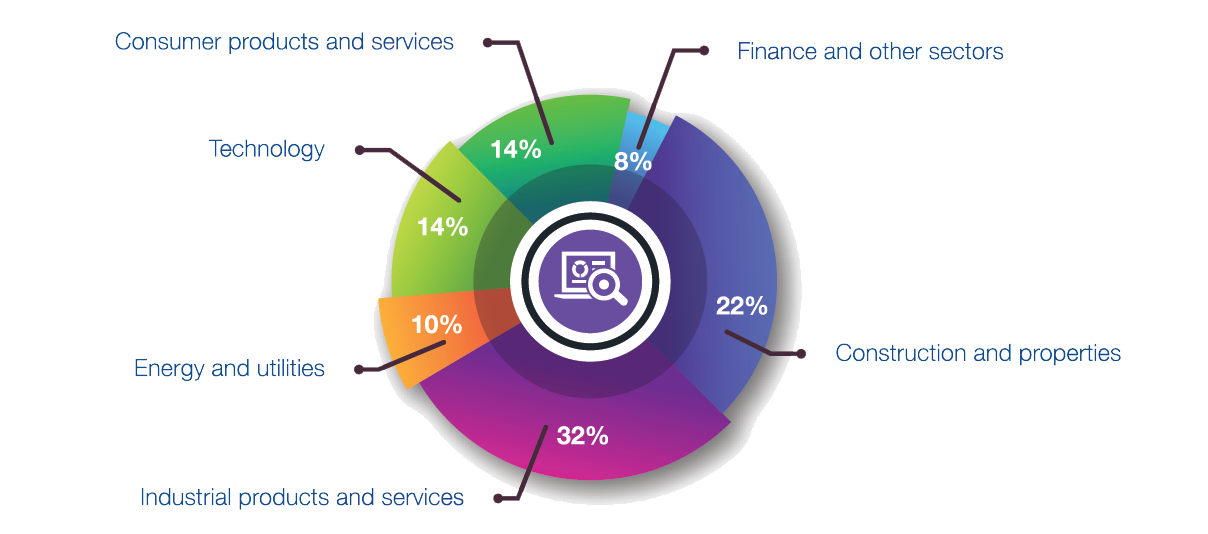

INDUSTRIES COVERED BY THE AOB’S INSPECTION IN 2022