The Guidelines on Continuing Obligations for Registered Auditors (Guidelines), which set out the obligations that

must be adhered to by a registered auditor, was issued in 2023. This is pursuant to section 31E(1)(a) of the Securities

Commission Malaysia Act 1993 (SCMA), where the responsibilities of the AOB include implementing policies which

contribute to an effective audit oversight system in Malaysia.

The objective of these Guidelines is to strengthen the framework for registered auditors and ensure better monitoring

and supervision of the registered auditors.

The Guidelines also consolidate the annual reporting obligations mandated via circulars on the registered auditors. The

Guidelines set out, among others, the following requirements:

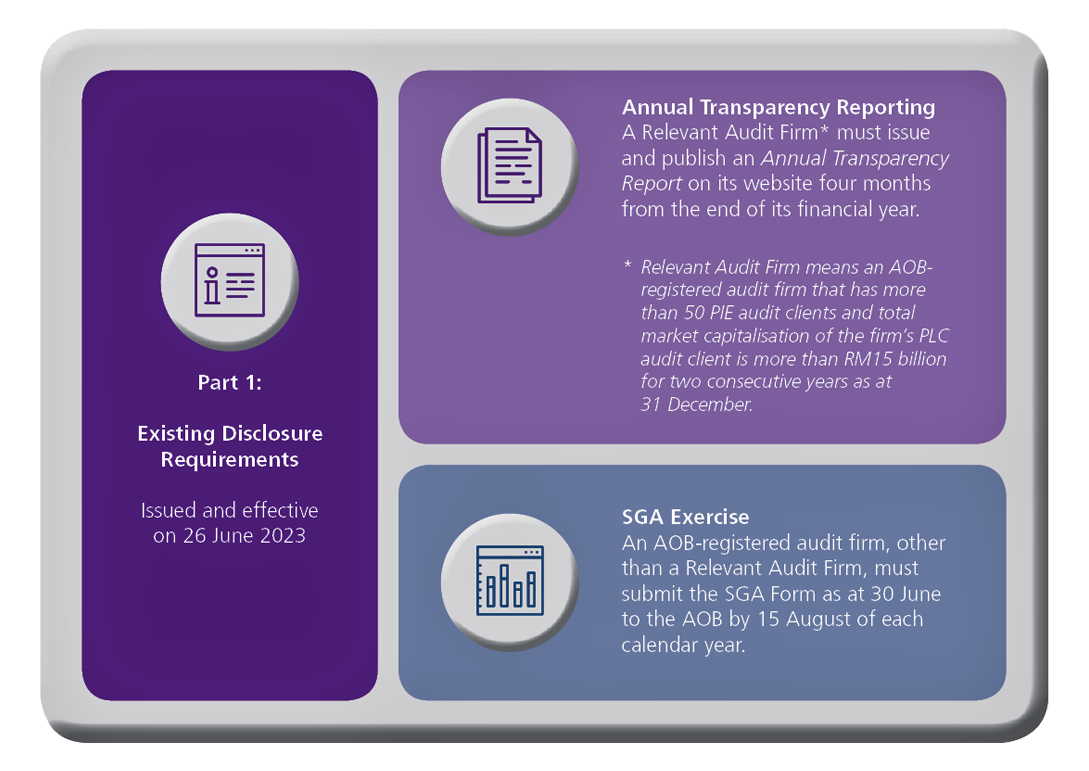

Part 1 of the Guidelines

(a) Annual Transparency Reporting

Issuance and publication of the Annual Transparency Report by audit firms (only firms that meet the reporting criteria) on its website to provide information on the governance structure of the audit firm, measures taken by the audit firm to uphold audit quality, and information on the audit firm’s audit quality indicators.

(b) Statistics Gathering and Analysis Exercise

Submission of the Statistics Gathering and Analysis (SGA) Form as prescribed by the AOB containing financial, client, human resources, and training information.

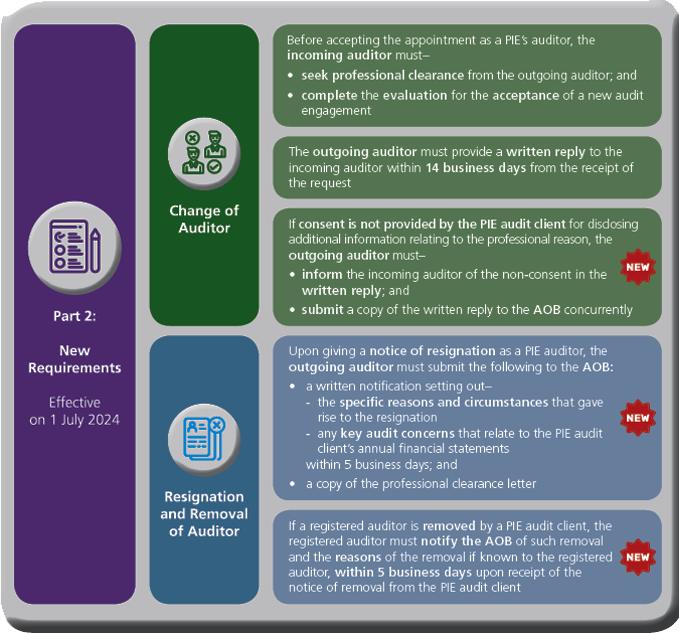

Part 2 of the Guidelines

(c) Change of Auditor

Professional clearance by the outgoing auditor to the incoming auditor when there is a change of auditor.

(d) Resignation and Removal of Auditor

Submission of a written notification by the auditor on reasons relating to its resignation and removal as an auditor to the AOB.

Auditors must ensure–