TABLE 1

Registration and recognition

As of 1 January 2025 | No. of new applicants | No. of withdrawals | No. of suspension | As of 31 December 2025 | |

|---|---|---|---|---|---|

| Registered | |||||

| Audit firm | 37 | 1 | (1) | (1) | 36 |

| Individual auditor | 377 | 29 | (23) | (2) | 381 |

| Recognised | |||||

| Audit firm | 5 | 1 | (1) | - | 5 |

| Individual auditor | 16 | 7 | (7) | - | 16 |

In 2025, the AOB suspended one audit firm and two individual auditors for two years due to their failure to comply with relevant requirements in ISQM 1 and ISAs.

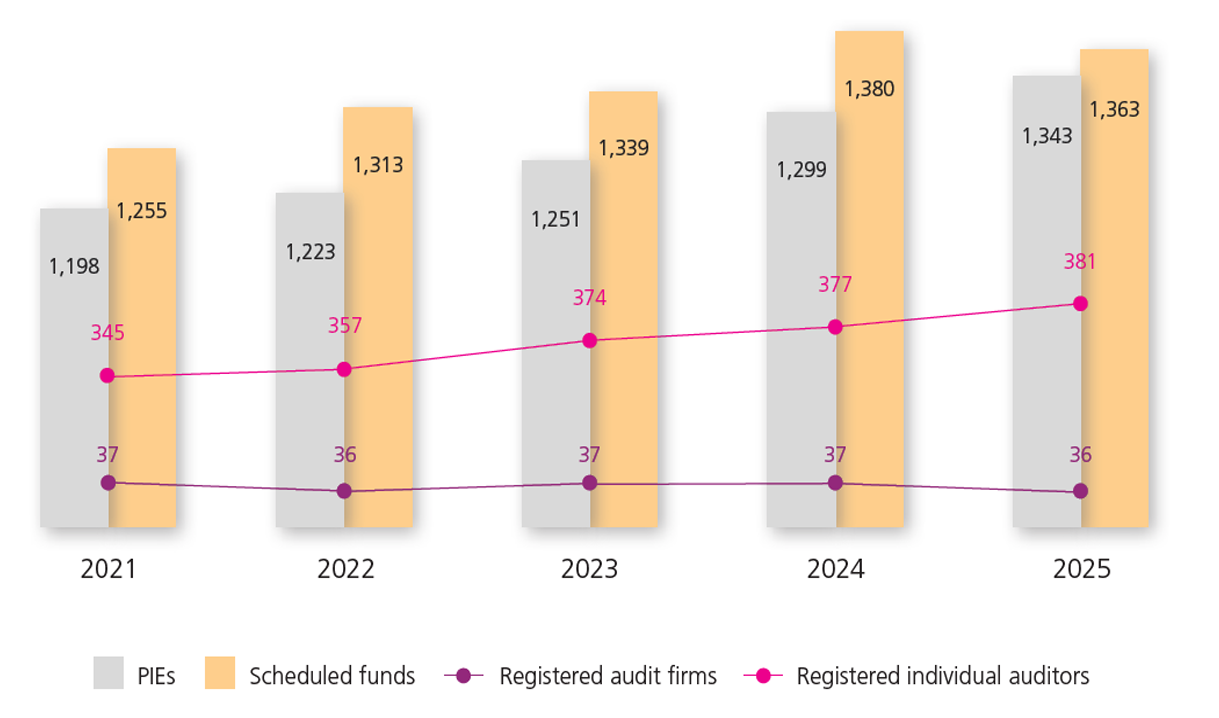

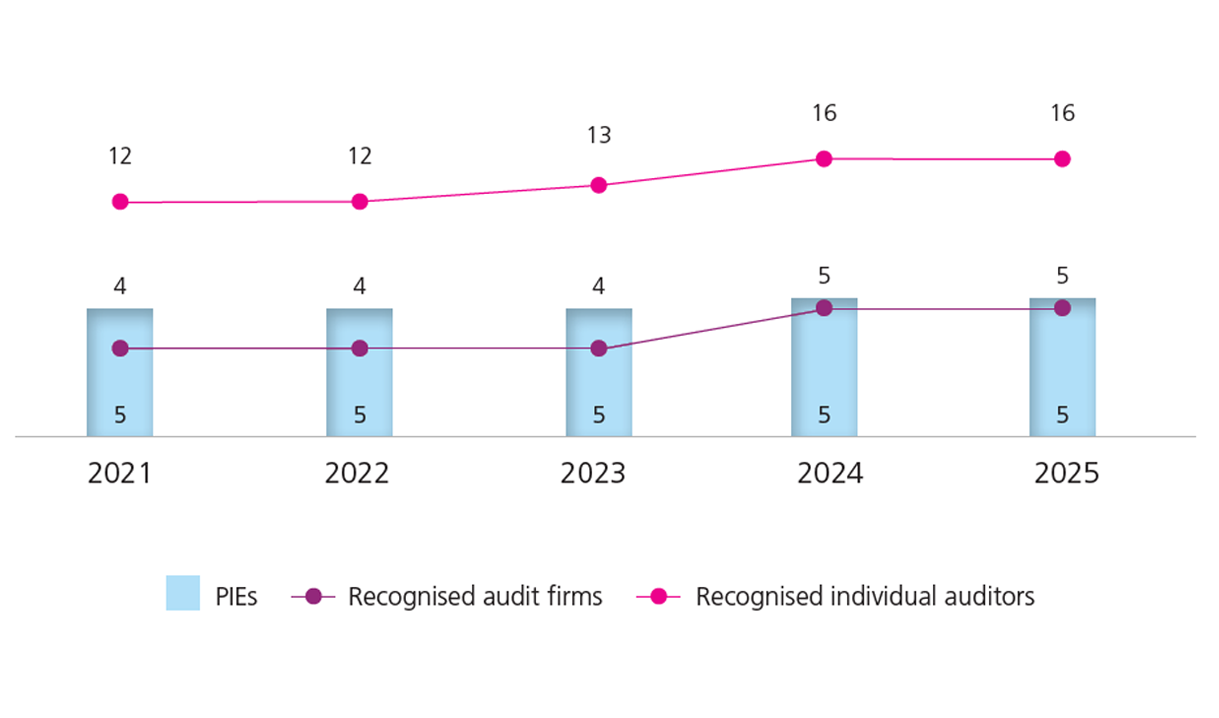

Chart 1 and 2 further depict the number of audit firms and individual auditors registered and recognised with the AOB as well as the number of PIEs audited for the last five years.

CHART 1

5-year registration statistics of registered audit firms and individual auditors

CHART 2

5-year recognition statistics of recognised audit firms and individual auditors

Readmission of persons with adverse comments as AOB-registered auditors

The AOB’s registration requirement and criteria is aimed at ensuring that only suitable individuals are registered as auditors of PIEs and schedule funds. This is to safeguard audit quality and to protect public interest.

The AOB’s fitness and probity assessment is guided by the Securities Commission Malaysia Act 1993 (SCMA), the AOB’s Handbook for Registration or Recognition and related guidelines. The criteria generally cover three broad pillars which include:

a) Character and Integrity

b) Competence and Capability

c) Financial Soundness