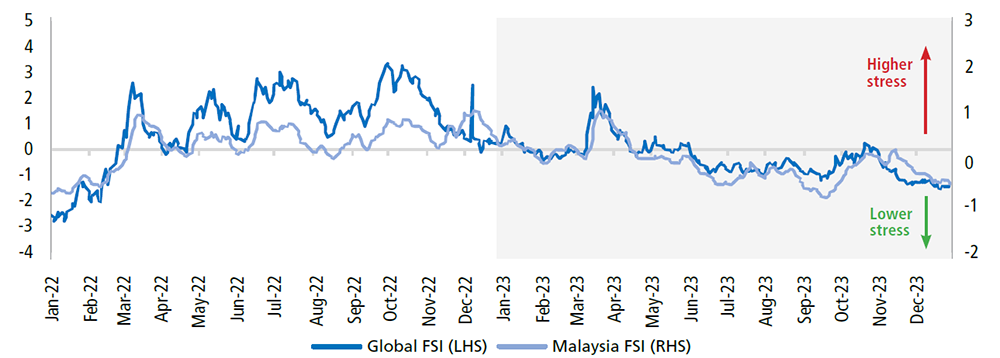

chart 1

Both global and Malaysian financial stress levels moderated in 2023, reflecting a shift in expectations that major central banks are approaching the peak of their tightening cycle, especially towards the end of the year

Global financial markets performance ended 2023 on a high note, despite the constant shifts in investor sentiments amid heightened global economic uncertainty. Disinflation progress in major economies also continued to influence expectations surrounding the path of global monetary policy, which resulted in volatility in global financial markets throughout the year. The overall level of global financial stress increased in March 2023 amid banking system stress in the US and Europe, but subsequently eased towards the end of the year following a shift in expectations that global interest rates are nearing their peak (Chart 1).

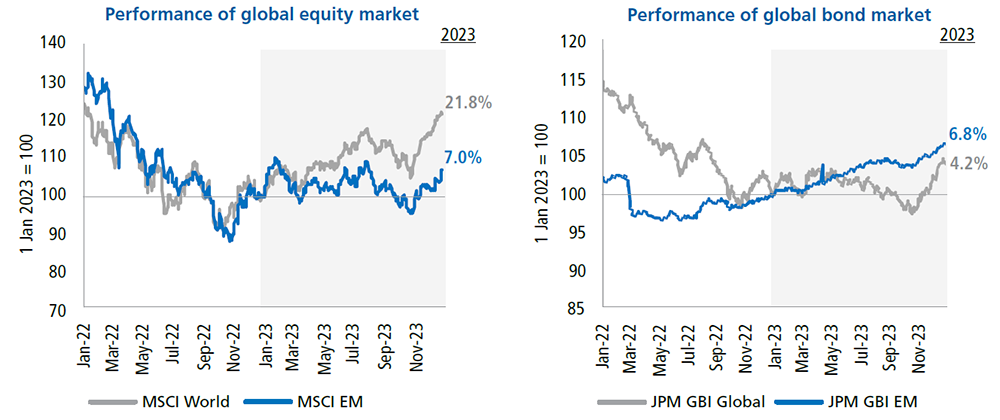

In the global equity markets, the MSCI World Index rose by 21.8% in 2023, while the MSCI Emerging Markets Index trailed the global benchmark by rising 7.0%, partly reflecting concerns from China’s subdued economic recovery. Meanwhile, global bond indices improved, particularly in the latter part of 2023, driven by dovish shift in monetary policy expectations amid the gradual easing in global inflationary pressures (Chart 2).

CHART 2

Global equities and bonds performances improved in 2023