chart 3

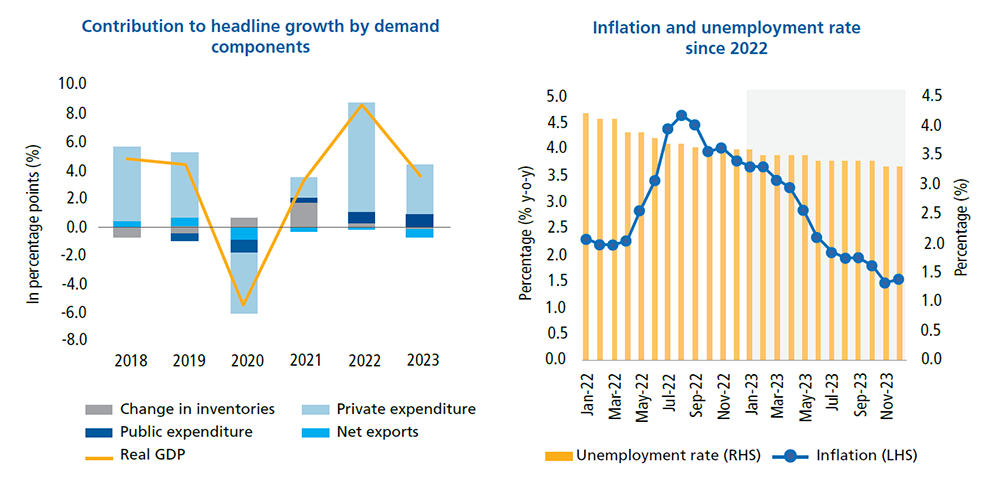

The Malaysian economy continued to grow in 2023 on the back of sustained resilience in domestic demand, amid challenging global trade conditions

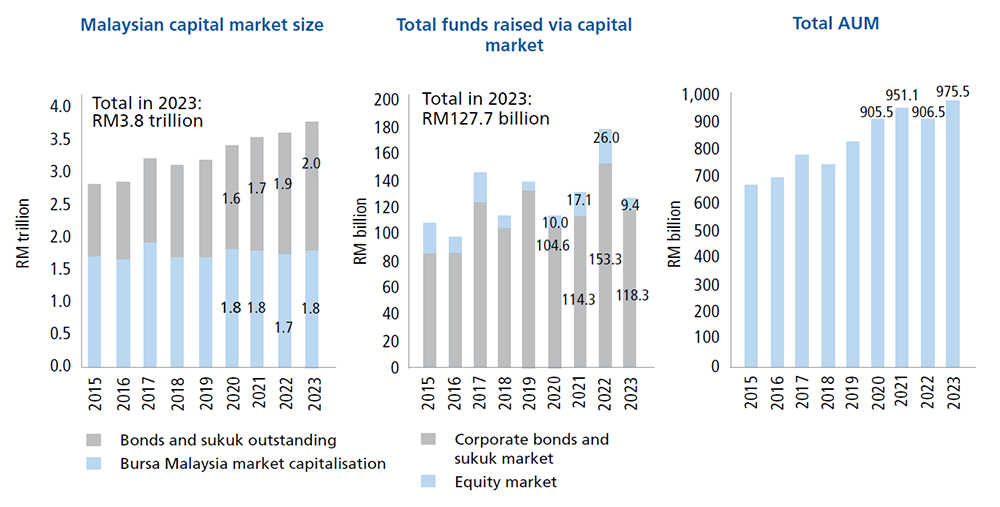

The Domestic Capital Market Continued to Support the Real Economy

chart 4

Size of the Malaysian capital market grew in 2023, despite lower fundraising activities, while AUM of the fund management industry registered a new high

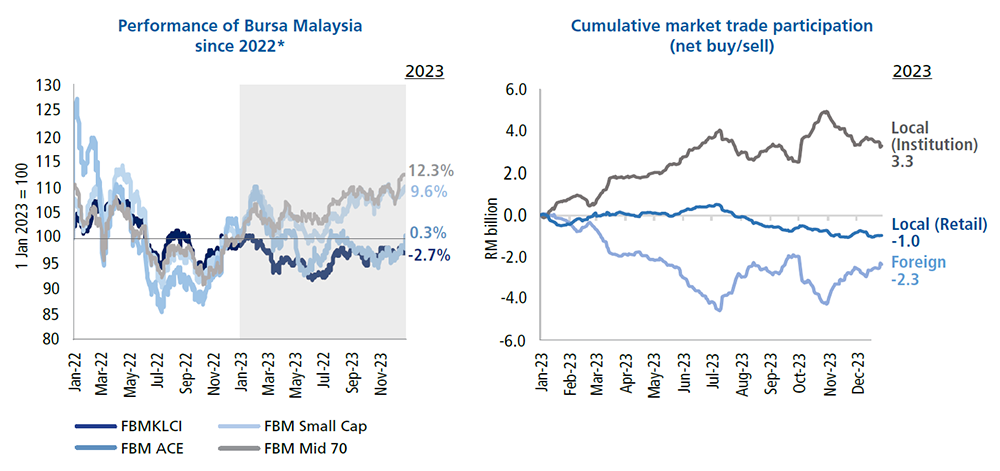

chart 5

Malaysia’s equity market experienced a positive shift in sentiment toward the mid and small cap segment, while local institutional investors turned net buyers of local equities

Note: * FBMKLCI consists of the largest 30 companies ranked by full market capitalisation in the FTSE Bursa Malaysia EMAS Index, while FBM Mid 70 encompasses the next 70 largest companies. FBM Small Cap consists of all constituents of the FTSE Bursa Malaysia EMAS Index that are not constituents of the FTSE Bursa Malaysia Top 100 Index. FBM ACE includes companies listed on the ACE Market.

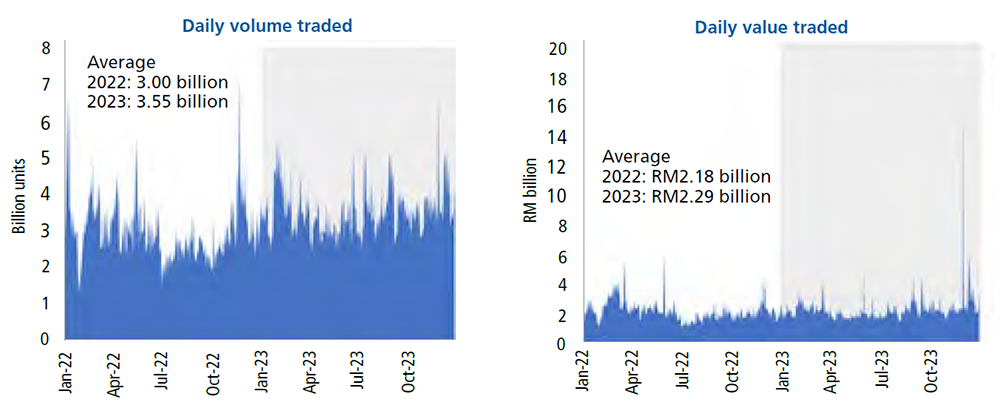

chart 6

Equity daily trading volume and value increased towards the end of the year amid improved investor sentiments

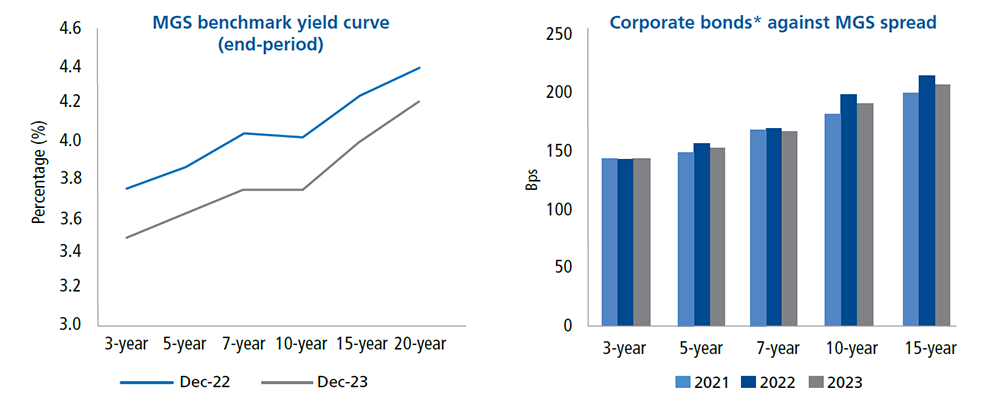

chart 7

The MGS yield curve shifted downward amid expectations of a stable domestic interest rate environment, while corporate spreads narrowed on resilient investor demand