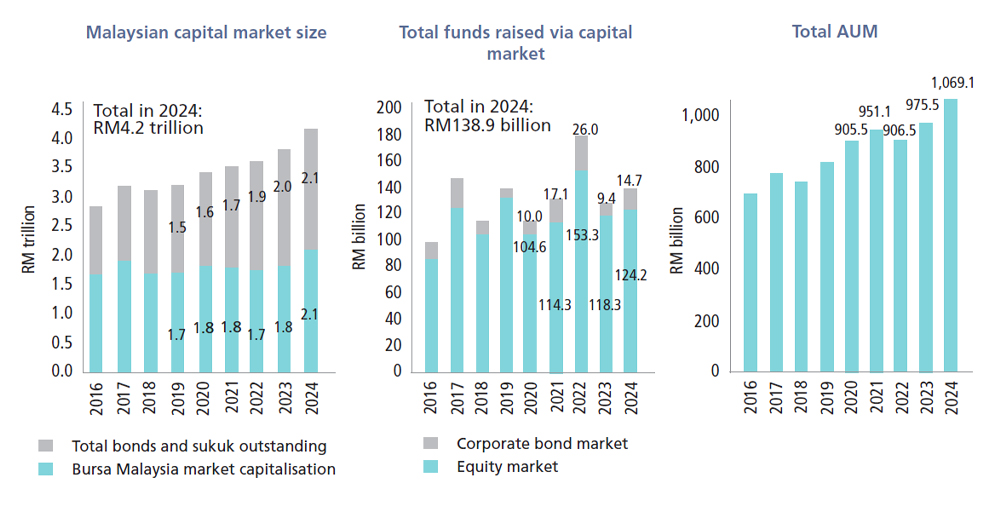

Total funds raised in the capital market grew to RM138.9 billion in 2024 (2023: RM127.7 billion), of which RM14.7 billion was raised through the equity market

2, while RM124.2 billion was issued through the corporate bond market. For the year, the number of IPOs increased to 55, from 32 in 2023. In line with the government’s economic policies that also focus on sustainability, the steady increase in issuances of sustainability-related instruments

3 affirmed the capital market’s pivotal role in supporting financing needs. Meanwhile, the growth in alternative fundraising platforms,

4 such as equity crowdfunding (ECF) and peer-to-peer financing (P2P financing), continued to promote financial inclusivity especially for micro, small and medium-sized enterprises (MSMEs).

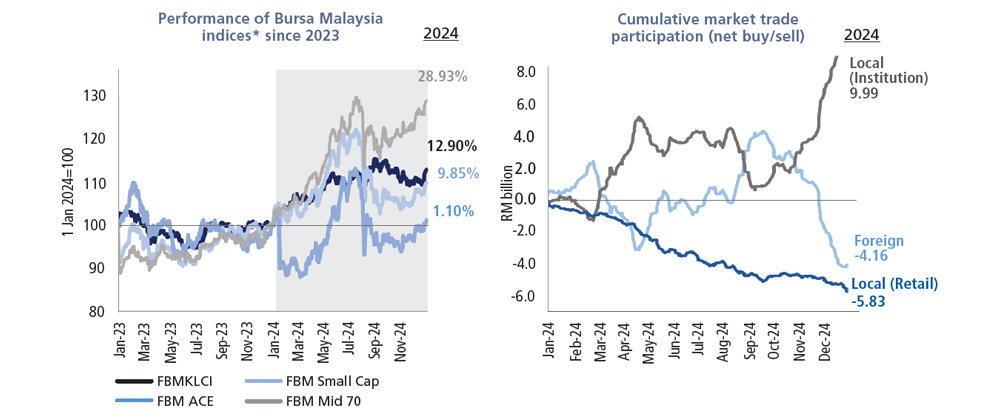

The performance of the Malaysian equity market was largely driven by a series of domestic factors including further clarity in national policy rollouts (e.g. NIMP 2030, NETR, NSS), fiscal consolidation measures (e.g. diesel subsidy rationalisation), favourable earnings growth and corporate activities. This was further supported by Malaysia’s position in the global semiconductor value chain and numerous analysts’ upgrades on their FBMKLCI targets. Besides domestic developments, global headwinds also continued to influence investment sentiment and redirection of capital, with volatility driven by the uncertainty of the direction and pace of global monetary policy in 1H2024, ongoing geopolitical conflicts and slower economic growth from China. Notably, the foreign equity outflow from the domestic equity market amounted to -US$941.9 million in 2024, compared to a net outflow of -US$514.2 million in 2023.

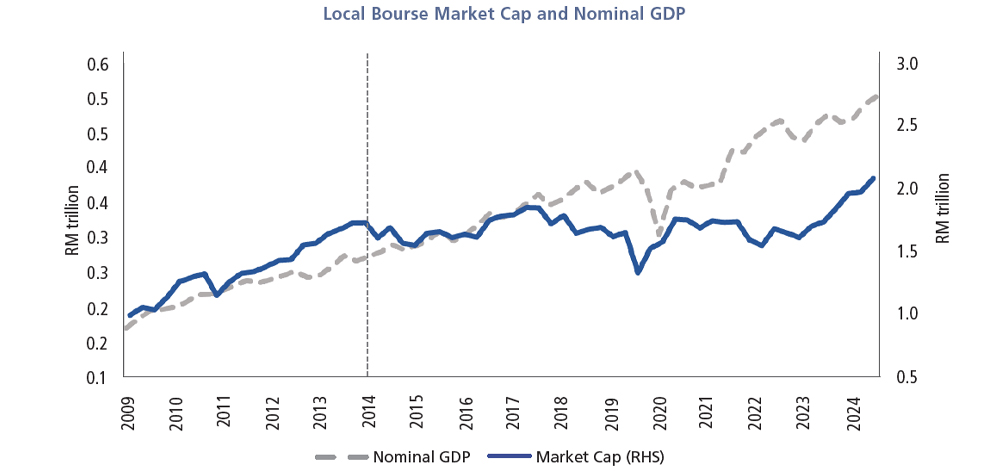

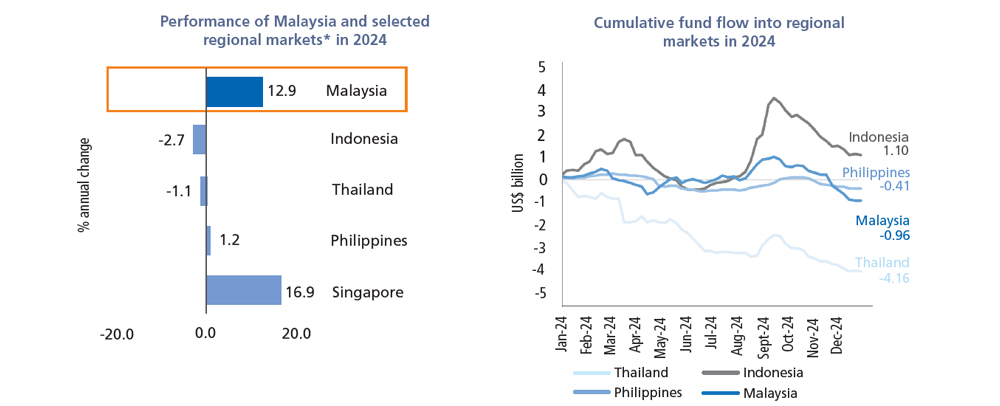

The overall market capitalisation of the local bourse ended higher at RM2.1 trillion in 2024 (2023: RM1.8 trillion), while that of the FBMKLCI rose to RM1.2 trillion (2023: RM1.0 trillion). The benchmark FBMKLCI index outperformed global and regional markets (MSCI Asia Pacific: 7.23%, MSCI ASEAN: 7.67%), rising by 12.90% (2023: -2.73%) to end the year at 1,642.33 points, while the FBM Mid 70 and FBM Small Cap rose by 28.93% and 9.85% (2023: 12.28% and 9.57%) to 18,841.13 points and 17,963.66 points respectively, displaying a positive shift in sentiment favouring medium and small-sized companies, as reflected by the favourable performances of FBM Mid 70 and FBM Small Cap (Chart 6). Notably, among ASEAN-5 counterparts, the FBMKLCI outperformed most of its peers despite recording a net outflow of funds (Chart 7). The growth in the equity market capitalisation for the year was favourable, in tandem with the pick-up in GDP growth. There continues to be a divergence in size of the capital market and GDP, but the capital market have made significant strides to narrow the gap in the past two years (Chart 5).