Suggested Searches

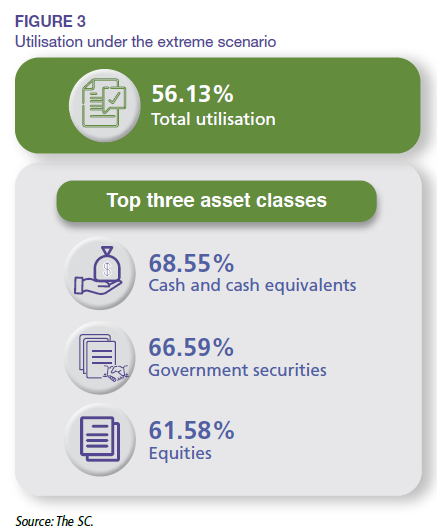

Based on the stress test results, it was found that investment funds would have to liquidate in aggregate 56.13% of their assets to satisfy redemption pressures based on the extreme scenario (Figure 3). Each of the top three asset classes (cash and cash equivalents, government securities and equities, in terms of liquidity order) experienced liquidations in excess of 60%. CIS saw 32.64% liquidation, followed by corporate bonds/ sukuk at 26.54%, primarily due to the extreme redemption scenario imposed.

Utilisation of liquidity buffers remained unlikely across all scenarios. Under the extreme scenario, the macro stress test showed adequate holdings of cash and cash equivalents and equities asset classes prior to any potential use of buffers, indicating ample liquidity in the portfolio structure.

Collectively, investment funds held approximately 10.17% of Bursa Malaysia’s total market capitalisation. In the extreme scenario, the SC estimated that severe disruption of the equities market is unlikely, given that redemption pressures were not expected to occur simultaneously.

In the fixed income asset class, investment funds held approximately 5.00% of the total outstanding domestic corporate and government bonds/sukuk. Nonetheless, the utilisation of this asset class to meet redemption was noted to be minimal particularly for corporate bonds/ sukuk, which remained lower in the liquidity order. Therefore, it is less likely to pose a severe risk transmission.

The most vulnerable funds have been identified as equity and mixed assets funds due to their high exposure in equities (around 90%) and lower level of liquid assets (below 3%). This high exposure in equities coupled with the low levels of liquid assets in these funds could exacerbate the risk of fire sales in the extreme liquidation scenario. Nevertheless, if liquidity risk management tools are implemented adequately and in a timely manner, this risk would be mitigated