Suggested Searches

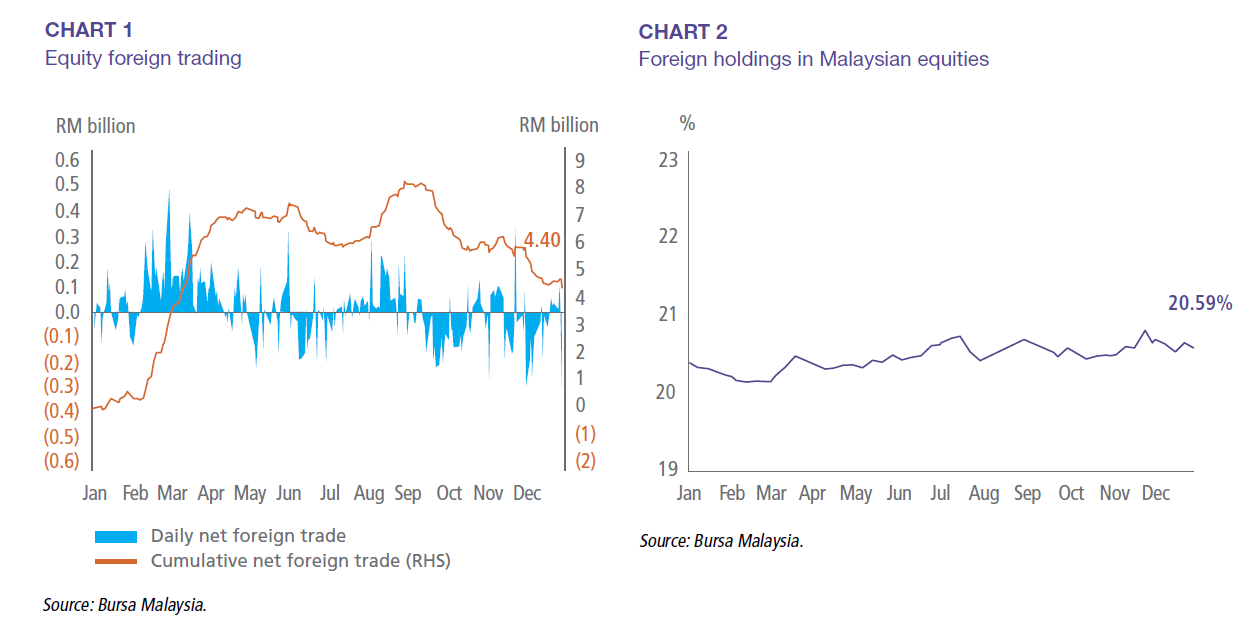

For equities, local institutional investors were net sellers with an outflow of -RM6.53 billion in 2022 (2021: net sell -RM9.06 billion), while buying support came from both foreign investors and local retail investors. Local retail investors’ net purchases were relatively muted with inflows of RM2.13 billion (2021: net buy RM12.21 billion) while foreign investors turned net buyers with inflows of RM4.40 billion in 2022 (Chart 1) (net sellers in 2021: -RM3.15 billion). As such, foreign equity holdings increased to 20.59% as at December 2022 (Chart 2) compared to 20.41% in 2021.

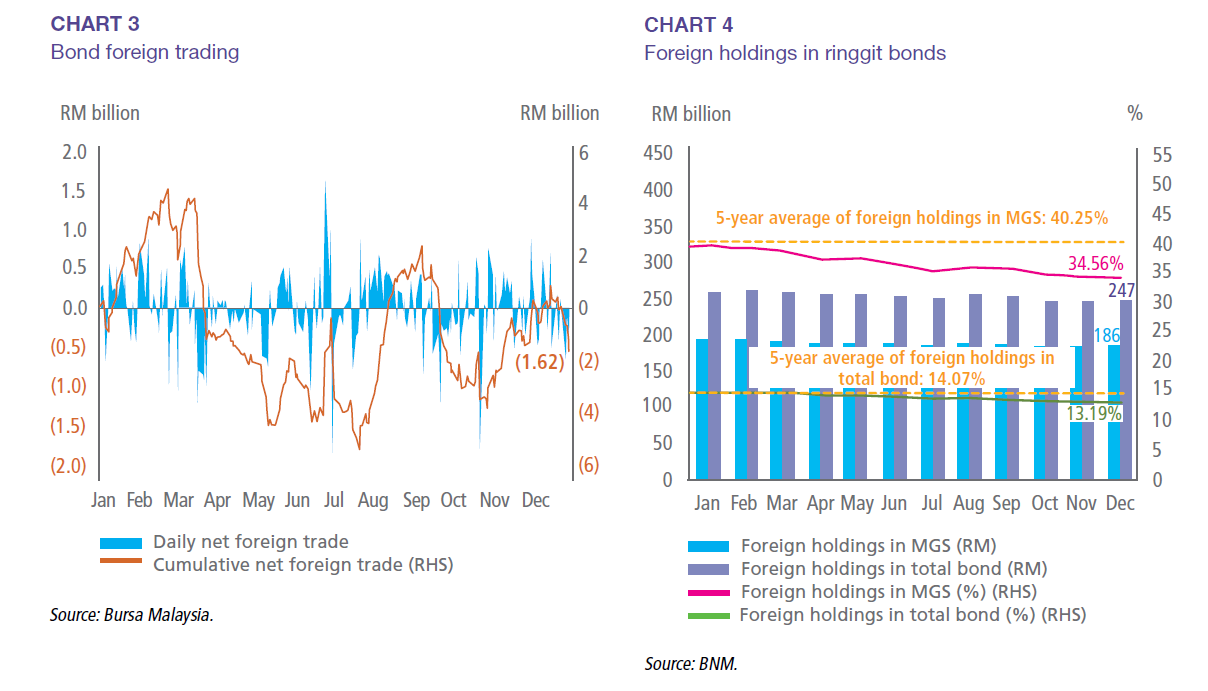

Foreign investors’ bond trading activity recorded a net outflow of -RM1.62 billion in 2022 (Chart 3) (net inflow in 2021: RM32.00 billion) led by MGS (-RM6.83 billion). Foreign demand for MGS and Government Investment Issue (GII) reduced in 2022 amid the continued hawkish stance of the Fed, with the narrower differential between MGS and US Treasury yields reducing the appeal of ringgit bonds for foreign buyers.

Foreign holdings in the Malaysian bond market stood at 13.19% (2021: 14.74%) as at December 2022, dropping below its 5-year average of 14.07% (Chart 4). The foreign investors held mostly MGS (75.36%, 2021: 73.85%), followed by GII (16.29%, 2021: 17.34%), Malaysian Treasury Bills and Malaysian Islamic Treasury Bills (2.85%, 2021: 3.07%) and corporate bonds and sukuk (5.50%, 2021: 5.73%).

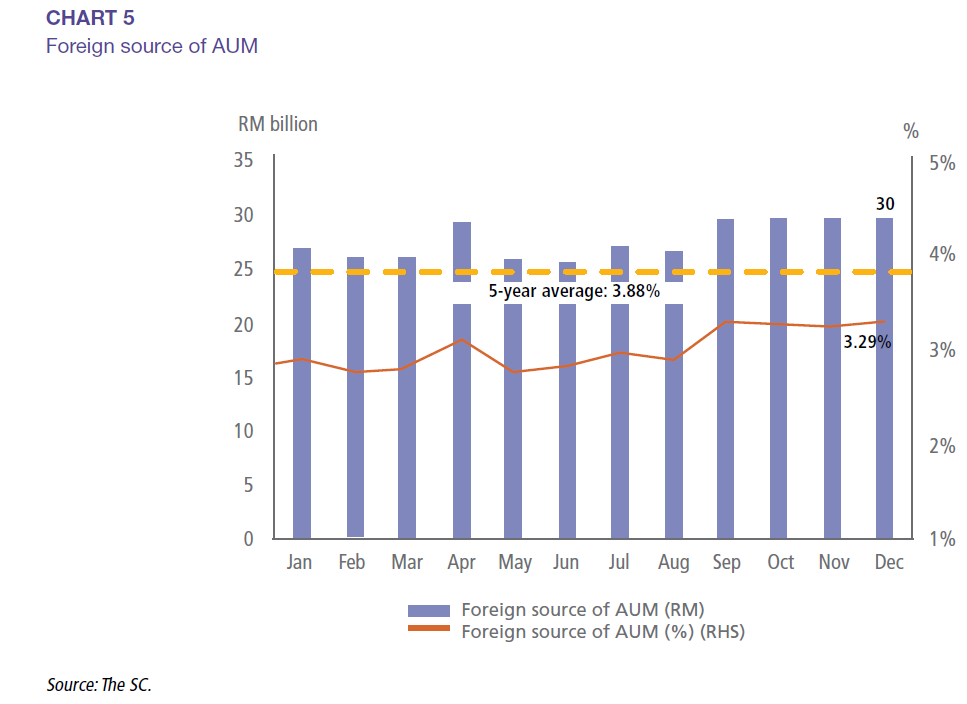

In the fund management segment, foreign investors made up 3.29% of total AUM as at end December 2022 (Chart 5) (2021: 2.81%). Foreign source of funds remained relatively small in this sector.