Suggested Searches

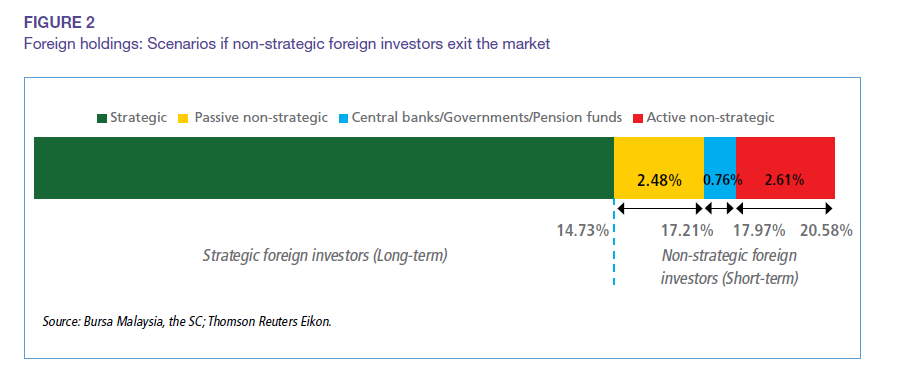

There were three hypothetical scenarios to simulate the possible foreign shareholding if non-strategic investors were to exit the domestic equity market. Figure 2 shows foreign investors arranged according to their likelihood of exiting the market in the event of a shock, with the least likely on the furthest left and most likely on the furthest right. Should active non-strategic investors excluding central banks, governments, and pension funds exit, the foreign holdings remaining were estimated to be around 17.97% (-RM50.95 billion outflow), down from 20.58%. Following that, if all active non-strategic investors exit the market, the foreign holdings would decline to an estimated 17.21% (-RM65.19 billion outflow). Subsequently, if all non-strategic investors, passive and active, were to exit the market, the foreign holdings after outflow would decrease to an estimated 14.73% (-RM109.74 billion outflow).

However, the likelihood of the three extreme simulations occurring is low. COVID-19, as measured by the heightened volatility of equity trading from February 2020 to May 2020, only led to a total equity outflow of -RM13.2 billion. In addition, there was sufficient liquidity in the market to facilitate trading activities in the event of any major selling.