Suggested Searches

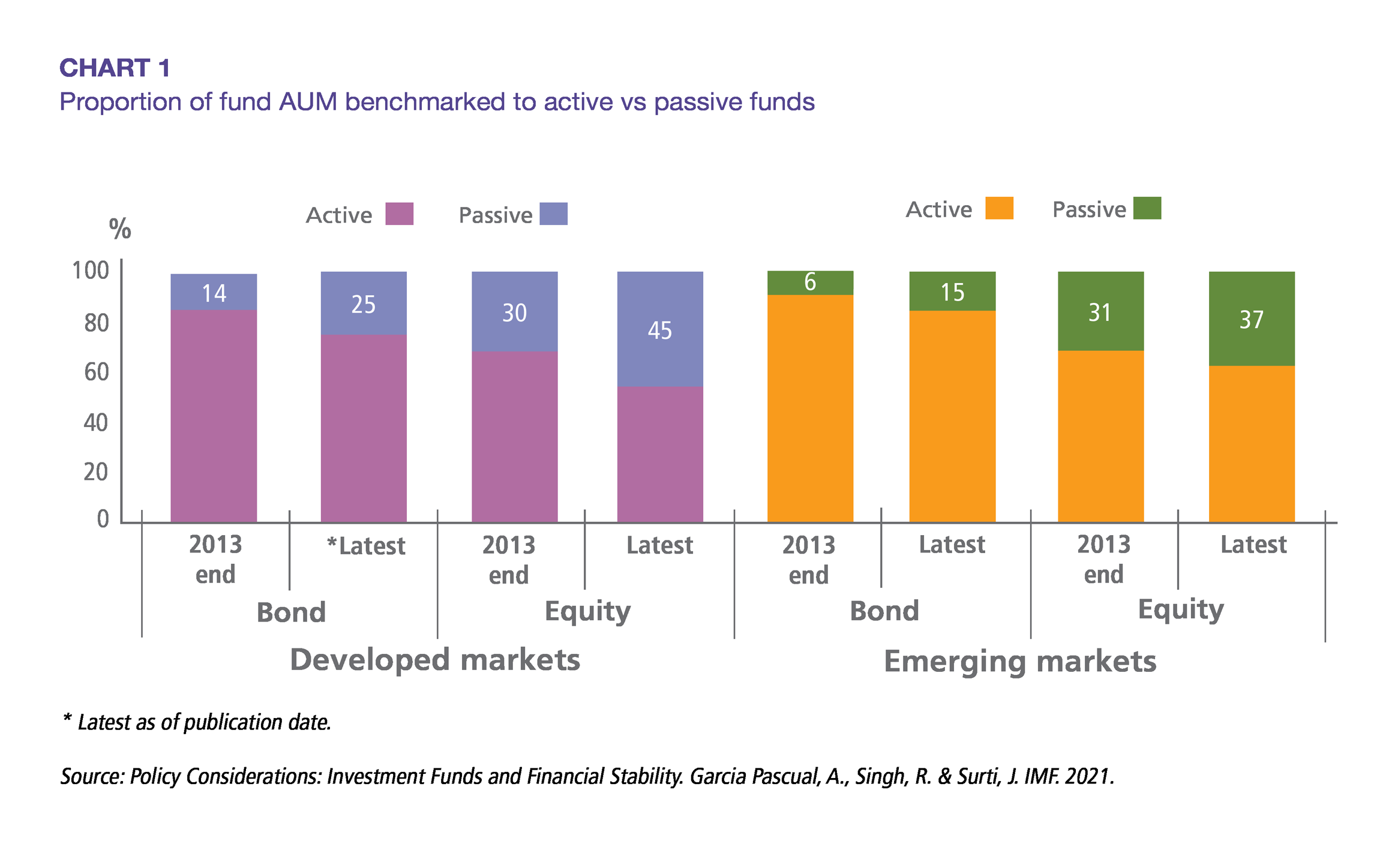

Passive funds such as index funds and exchange-traded funds (ETFs) are benchmark-driven and track components of market indices. Such passive funds maximise returns by replicating a representative benchmark. The appeal of passively managed funds lies in their diversified and low-fee portfolios, which in some cases outperform their actively managed counterparts.

Passive investing, together with technological changes and the use of data, have the potential to change the way that securities markets function and market participants interact. Given their tracking of benchmark indices, passive fund weightages could influence the presence of foreign investors in a country. The addition of a PLC to an index would result in an inflow of investment from funds tracking the index, benefiting the domestic capital market.

Globally recognised indices that track Malaysia include the MSCI Emerging Markets Index, FTSE Emerging Index, and the Nasdaq Emerging Markets Index. The MSCI Emerging Markets Index comprises large and midcap representation across 24 emerging market countries, covering almost 12% of the world market capitalisation. Malaysia’s securities weightage in the MSCI Emerging Markets Index was 1.52% as of 30 September 2022.

In the US, Bloomberg Intelligence reported that it is only a matter of time before passive assets overtake active assets in mutual funds and ETFs. As of December 2020, approximately 42.9% (US$10 trillion) of US-based mutual funds and ETFs were passively managed which were up from 31.6% (US$4.1 trillion) at the end of 2015, demonstrating the rapid growth of passive funds. For emerging markets, there was a 5% increase in AUM benchmarked to the MSCI Emerging Markets Index from December 2016 to December 2021. In Malaysia, it was estimated that RM41.85 billion or 40.59% of foreign non-strategic investors were passive investors who tracked index funds in general. In this regard, Malaysian PLCs included in an index would be appealing to passive funds. Thus, the shifting trend from active to passive investing intensifies the need for PLCs to be competitive in terms of size and liquidity.

The IMF in its Global Financial Stability Report issued in April 2019 highlighted that while inclusion in an index provides emerging market countries with access to a larger and more diverse pool of financing, inflows are highly sensitive to global or regional factors common to emerging markets included in the index. Investors are inclined to treat emerging markets as an asset class rather than focus on country-specific developments. Consequently, any adverse news to emerging markets as a group may cause destabilising effects to a country with a larger share of benchmark-driven investments.

There could also be systemic stability concerns when rebalancing is being carried out by leveraged or inverse ETFs as it could potentially cause adverse price movements. The increasing use of passive-index and benchmark-hugging-active investment strategies to invest in high-risk, low-liquidity assets might exacerbate first-exit incentives by increasing the likelihood of fire-sales under stress.1 Given the concerns, the increase in passive funds has prompted comprehensive discussions between index providers, regulators, and investors. In addition, enhanced transparency by index providers in terms of eligibility criteria would also improve flow volatility management.