Suggested Searches

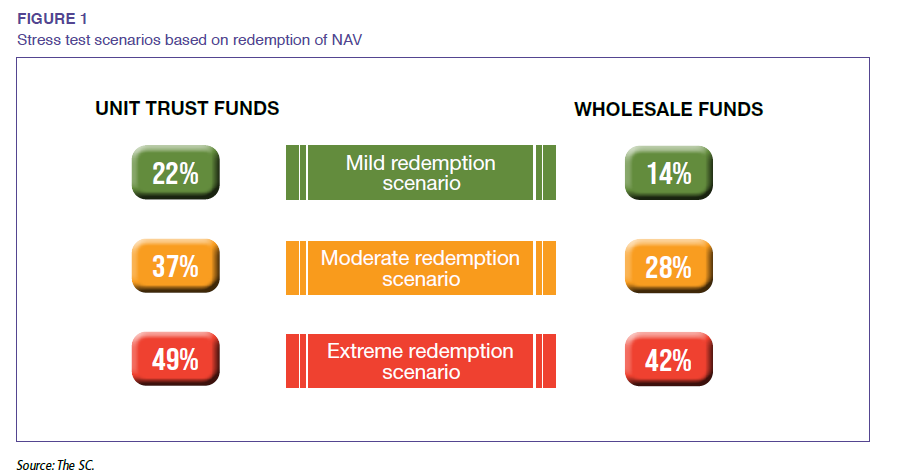

The macro stress test was conducted based on plausible tail scenarios, which were derived from historical redemption data to simulate mild, moderate, and extreme redemption pressures (Figure 1). Several assumptions were applied in developing the scenarios, including the expectation that the initial redemption shock would prompt further redemptions by other unitholders. Additionally, individual investment funds were required to maintain liquidity buffers of at least 10% in all asset classes in anticipation of future redemptions by unitholders. Effectively, funds incapable of reserving sufficient buffers for redemption are considered illiquid. The stress test exercise also assumed that neither the regulator nor the trustee would intervene in terms of liquidity management practices.

The macro stress test model involved a bottom-up approach where risks across the financial markets and assets were considered. The model utilised sensitivity analysis where a factor of large rolling redemption pressures was applied to the individual investment funds liability in three broad scenarios of redemption pressures based on historical redemption patterns. On the funds’ asset side, liquidation of certain asset classes was moderated by downward pressure on asset prices.

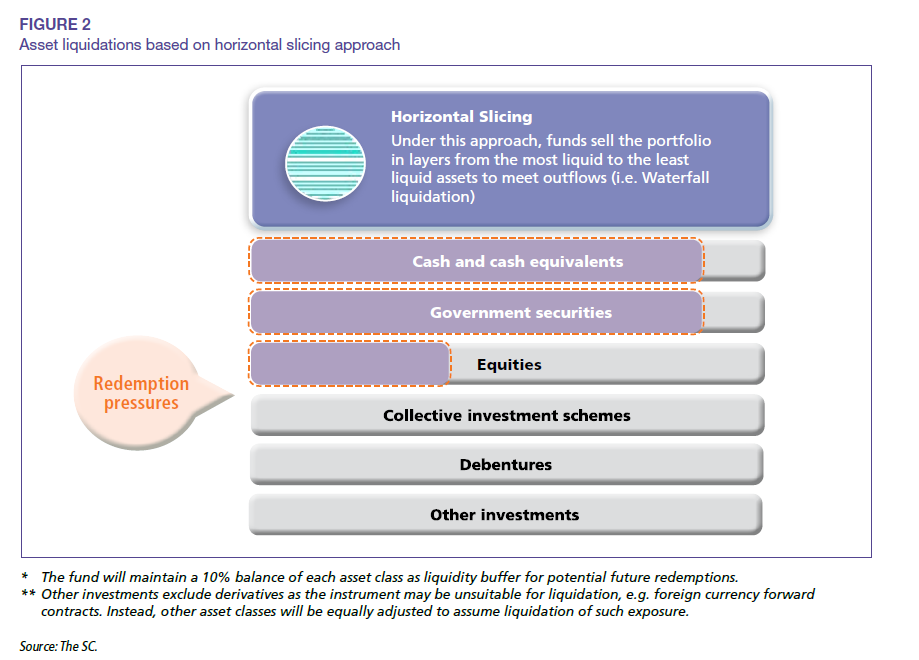

In terms of liquidation, a macro stress test can be conducted based on either one of two slicing approaches. In a horizontal slicing2 (waterfall liquidation3) approach, liquidation takes place from cash and cash equivalents (most liquid) to corporate bonds/sukuk (least liquid). Under the vertical slicing (pro rata liquidation) approach, the structure of the portfolio takes precedence; all securities are liquidated in the same proportion. Such strategies would enable fund managers to maintain their respective asset allocations.

Under the SC’s macro stress test, the horizontal slicing approach was chosen given its capacity to render a more pronounced observation into potential risk transmission effects across major asset classes. In this slicing approach (as illustrated in Figure 2), liquidation would first occur in withdrawals of highly liquid assets, including cash, deposits, money market placements, and government securities.

To simulate the impact of a market risk shock at the point of liquidation, the stress test model assumes a decline in fair value for the equities, government securities, and corporate bonds/sukuk asset classes.